Q1 2024 - A Market Review

A stellar quarter brought stocks back into record territory after two years even as the Magnificent Seven began to break apart.

The 2023 rally continued into Q1 2024 as a positive combination of stable economic growth, falling inflation, impending Fed rate cuts and ever-growing enthusiasm towards artificial intelligence (AI) propelled stocks higher, as the S&P 500 rose above 5,000 for the first time and then continued to hit new all-time highs.

The year began with a modest uptick in volatility, as traders and investors initially booked profits following the strong 2023 gains. However, those initially small declines intensified shortly after the start of the year when the December Consumer Price Index (CPI) measure of retail inflation declined less than expected.

That reading challenged the idea that inflation was quickly falling towards the Fed’s 2.0% target and caused investors to delay the expected date of the first Fed rate cut, as expectations for that first cut shifted from March to June. Fears of potentially higher-than-expected rates pushed stocks temporarily into negative territory early in January. However, the declines didn’t last.

First, Q4 corporate earnings were again better than feared and that helped stocks recover from those early declines. Then, in late January, the Federal Reserve clearly signaled that rate hikes were over and strongly hinted that rate cuts would occur in the coming months. Investors seized on that positive message and the S&P 500 hit a new all-time high late in the month and finished with a modest gain, up 1.59%.

The rally accelerated in February as fears of a potential rebound in inflation subsided. Inflation metrics released in February largely met expectations and importantly did not imply that inflation was reaccelerating. As such, investor expectations for a June rate cut were strengthened and that helped stocks extend the year-to-date gains.

Then, on February 21st Nvidia, the semiconductor company at the heart of the AI boom, posted much-stronger-than-expected earnings and guidance. Those results further fueled investors’ AI enthusiasm and large-cap tech stocks powered the S&P 500 higher into month-end as the index hit a new record high above 5,000. The benchmark domestic index gained 5.34% in February.

The final month of the quarter saw yet more gains, aided by familiar factors such as solid economic growth, generally as-expected inflation data, AI enthusiasm and bullish Fed guidance. Broadly speaking, economic and inflation data largely met expectations in March and continued to point towards stable growth and still (slowly) falling inflation.

Then, in mid-March, updated Federal Reserve interest rate projections still pointed towards three rate cuts in 2024, further reinforcing investor expectations for a June rate cut. Those positive factors combined with additional strong AI-related earnings reports to push markets broadly higher as the S&P 500 crossed 5,200 for the first time late in the month and ended March with strong gains.

In sum, the 2023 rally continued and accelerated in the first quarter of 2024 thanks to positive news flow that implied stable growth (no recession), still falling inflation, looming Fed rate cuts and continued AI enthusiasm and those factors propelled the S&P 500 to new all-time highs.

Q1 2024 Performance Review

The first quarter of 2024 reflected a much more evenly distributed rally compared to the fourth quarter of 2023, where tech and tech-aligned sectors handily outperformed the rest of the markets. Over the past three months markets saw broad gains distributed more equitably amongst various sectors and industries.

However, while the rally in stocks did broaden out in the first quarter, that did not really benefit Small Caps as they were some of the notable laggards over the past three months. Small caps registered a positive return for Q1 but lagged Large Caps as concerns about stubbornly high interest rates weighed on the smaller names, as they are more sensitive to higher funding costs and concerns about slowing growth.

From an investment style standpoint, growth once again outperformed value in the first quarter but the margin was much closer than last year, as both investment styles logged strong quarterly returns. Continued heightened AI enthusiasm was the main reason for the modest growth outperformance over the past three months, as Large Cap tech stocks again saw strong rallies in Q1.

The so-called Magnificent Seven stock club that powered the recent rally began to fracture as both Apple and Tesla had a poor Q1, with Tesla in particular having a torrid time, losing almost a third of its value over the course of the quarter.

On a sector level, as mentioned, gains were broad as 10 of the 11 S&P 500 sectors finished Q1 2024 with a positive return. Unlike 2023, however, tech and tech-aligned sectors didn’t substantially outperform. To that point, the best-performing sectors in the market in the first quarter were Communication Services, Financials, Energy and Industrials.

That sector mix reflected the influences of AI enthusiasm, strong financial stock guidance, solid U.S. economic data and rising optimism towards a potential rebound in Chinese economic growth. The diversified gains demonstrated that the Q1 rally was driven by a more varied set of influences beyond just AI enthusiasm.

Turning to the laggards, the only S&P 500 sector to log a negative return for the first quarter was Real Estate, as it continues to be weighed down by concerns about the health of the commercial real estate market. Specifically, terrible quarterly earnings from New York Community Bank reminded investors of the sustained weakness in the commercial real estate market and that weighed on the real estate space. Consumer Cyclical also lagged and registered only a slightly positive return as numerous retailers warned about a potential slowing of consumer spending during the first quarter (this is something to monitor closely as we begin the second quarter).

US Equity Indexes Q1 Return

Internationally, foreign markets posted solid quarterly gains but still underperformed the S&P 500. Looking deeper, foreign developed markets outperformed emerging markets in Q1 thanks to better-than-expected economic data and as expectations rose for early summer rate cuts from the European Central Bank and Bank of England.

Emerging markets, meanwhile, logged only slightly positive returns in Q1 2024 and solidly underperformed the S&P 500 thanks to mixed Chinese economic data and a lack of substantial Chinese economic stimulus early in the quarter.

International Equity Indexes Q1 Return

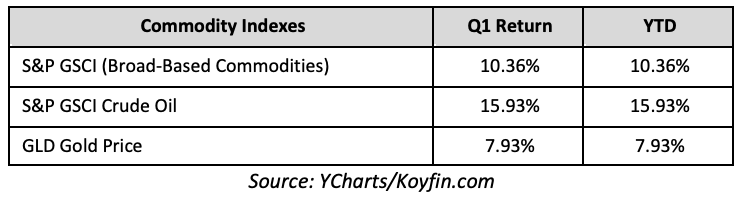

Commodities as an entire asset class saw strong gains in the first quarter thanks to still-elevated geopolitical tensions, a weaker U.S. Dollar and smaller-than-expected declines in inflation.

Oil rallied sharply in Q1 thanks to late-quarter optimism for an acceleration in Chinese economic growth, combined with an increase in geopolitical tensions following the continued attacks on commercial ships in the Red Sea, along with an increase in Russian attacks on Ukrainian energy infrastructure.

Gold hit a new all-time high, meanwhile, and logged solidly positive returns thanks to the aforementioned buoyant inflation data and a weaker U.S. Dollar.

Commodity Indexes Q1 Return

Switching to fixed income markets, the leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a slightly negative return for the first quarter of 2024. Disappointing inflation readings were the primary reason for the weakness in bonds as they delayed the expected start of Fed rate cuts from March until June and caused bond investors to consider that rates may be higher than previously expected over the medium and longer term.

Looking deeper into the fixed income markets, longer-duration bonds handily underperformed those with shorter durations. That performance gap was due to the slower-than-expected decline in inflation, because while it won’t materially delay the start of Fed rate cuts, it does threaten to keep rates “higher for longer,” which is a bigger negative for longer-dated debt.

Turning to the corporate bond market, higher-yielding but lower-quality “junk” bonds outperformed investment grade debt as looming Fed rate cuts and buoyant inflation, amidst stable economic growth, led bond investors to “reach” for more yield in the riskier parts of the credit spectrum.

US Bond Indexes Q1 Return

Q2 2024 Market Outlook

We begin the second quarter in the midst of a positive macroeconomic environment as growth appears stable, inflation is still falling, the Fed is likely going to deliver the first rate cut in four years and AI enthusiasm keeps earnings estimates high. But while this is undoubtedly a favorable set up, the strong rally of the last six months has left the S&P 500 at previously historically unsustainable valuations while investor and analyst sentiment is very bullish and, potentially, complacent. So, while the outlook is currently positive, it’s essential we continue to monitor the macroeconomic horizon for risks because at current stretched valuations and with sentiment very bullish, the market is highly vulnerable to a negative surprise.

Specifically, while it’s true that economic growth has remained resilient in the face of higher rates, some data is pointing to a possible loss of momentum. Retail sales missed expectations in January and February while the unemployment rate jumped to the highest level since 2022 during the first quarter. Neither number warrants immediate concern about the economy right now, but both serve as a reminder to watch data closely as a continued economic expansion is not guaranteed.

The scourge of inflation, meanwhile, is still retreating but the pace of that decline has slowed quite meaningfully. Core CPI, which the Fed takes notice of, has barely declined over the past several months as it sat at 4.0% annualized back in October and then in February was just 3.8%.

Meanwhile, other anecdotal indicators of inflation have hinted at a rebound in prices. If inflation bounces back that will reduce the number of Fed rate cuts in 2024 and that disappointment could pressure stocks and bonds.

To that point, markets fully expect a June rate cut from the Fed and a total of three rate cuts in 2024 and that assumption was central to the first quarter rally. However, those rates cuts are not guaranteed and if the Fed does not cut as aggressively or as frequently as markets expect, that will result in disappointment and a potential meaningful decline in stocks and bonds.

Finally, investor enthusiasm towards the potential for artificial intelligence remains a critical part of the bull market and strong earnings from Nvidia in February furthered investors’ hopes that AI integration will lead to a profitability and earnings boom, not just for tech companies, but for the entire market. However, that’s also not guaranteed and so far, AI integration has produced a lot of flashy headlines but not a lot of profit maximization for non-tech industries. If AI fails to broadly boost profits outside of its own little bubble and demand declines, that will be a significant negative for this market.

Bottom line, this historic rally is currently still supported by very positive fundamentals. But we cannot let the currently healthy setup blind us to risks and that’s why, while we are pleased with the market performance, we must recognize that this market remains highly vulnerable to negative news.

The past several years have demonstrated that a well-planned, long-term focused and diversified financial plan and investment strategy can withstand virtually any market surprise and related bout of volatility.

I remain constantly vigilant on behalf of Anglia Advisors’ clients regarding both portfolio risk and the economy and will continue to keep you informed of my opinions with my weekly market review every Sunday.

If you are already a client, I want to thank you for your ongoing confidence and trust. Please do not hesitate to contact me with any questions, comments or to schedule a portfolio review.

If you aren’t a client yet, please reach out and I’d be delighted to discuss bringing you into the Anglia Advisors family.

Simon Brady CFP® CETF®. Founder, principal Anglia Advisors.

WWW.ANGLIAADVISORS.COM | SIMON@ANGLIAADVISORS.COM | CALL OR TEXT: (929) 677 6774 | FOLLOW ANGLIA ADVISORS ON INSTAGRAM