Another weekend, another complete lack of progress or even any useful information related to the Iran war as the paralysis continued with both sides wasting everybody’s time and effort by offering up proposals that are clearly non-starters since they know full well the other side won’t accept them.

Wall Street loves itself a corny acronym and while bulls are tending to still hold on to the long-standing principle of TACO, many of the bears are adopting NACHO (Not A Chance Hormuz Opens).

All we really got was Trump barking that “the clock is ticking”. No shit, thought Wall Street traders who had been promised an end to all this uncertainty weeks ago. With inflation fire alarms starting to go off all over the world, markets made a cautious start to the week on Monday.

After Japanese interest rates were driven to the highest levels in history overnight, stock prices dipped in New York, led lower by recently-buoyant Big Tech names, with energy prices and US interest rates continuing to head north on slowly evaporating confidence in an imminent workable US/Iran pact.

Oil prices eased slightly late on as Trump implausibly announced that he had been talked out of resuming military strikes on Iran by Gulf allies pending some kind of unspecified deal, but Wall Street shrugged this off on Tuesday as just another tiresome and transparent negotiating ploy.

The first of the week’s impactful earnings reports came out with Home Depot disappointing. The indexes retreated further, again tech-fueled, with stock traders nervously eyeing the one-way traffic in bond markets that was sending longer term interest rates to highs not seen since Soulja Boy topped the Billboard charts.

Wall Street got another read on the American consumer with Target, TJ Maxx and Lowe’s earnings on Wednesday morning all beating estimates. There was nothing in the released minutes from the latest Fed meeting that indicated an imminent Fed Funds Rate cut, but they don’t seem to be overtly plotting a hike either, although the most commonly-expected next Fed move in 2026 has now flipped over from doing nothing to actually raising rates (see INTEREST RATE EXPECTATIONS below).

Stocks chose to take encouragement from the continued positive earnings environment and the indexes moved nicely higher, erasing the losses of the previous two days as oil prices drifted lower. Bonds had a much better session as interest rates pulled back from their recent highs. Nvidia’s earnings after the bell were perfectly good but lacked a wow factor and the stock did little in the after-market.

On Thursday, Walmart’s pre-market earnings, considered a good barometer of the state of lower-and-middle income consumers and the K-shaped economy, showed significant profit margin compression and the stock sank.

Combined with a muted reaction to Nvidia’s numbers and the continued endless foot-dragging and more unruly rhetoric from both sides of the Iran war spiking energy prices again, this sent the indexes slipping back into the red early on, but a late bout of dip-buying dragged them back up to close lightly in the green.

Stocks completed their eighth consecutive week of gains on Friday, the longest such streak for three years, as longer term interest rates and energy prices continued to recede on the hopes of some kind of a US/Iran settlement ticked a little higher based on still-hazy but slightly more upbeat pronouncements from both sides.

Some other things I’m thinking about ..

For AI-driven stock market growth to be sustainable the biggest tech companies will need to see a positive return on their colossal data center spending. If this fails to materialize because people and companies don’t use AI as much as expected or pay for its use, then the so-called hyper-scalers (Meta, Amazon, Oracle, Microsoft, Google etc.) will have to cut spending on them and that could badly damage the rest of the tech sector and thereby the tech-heavy US indexes. We won’t find out that out in the near term, but stock markets are currently acting like the answer can only be “yes, the spending will continue come what may,” and I’m not yet 100% convinced that’s definitely true beyond the next few quarters.

Trump’s job approval rating is cratering, consumer sentiment is at a horrendous multi-decade record low (even Republican voters are fuming) and inflation expectations are through the roof, just a few months before the midterms as Americans go into the Memorial Day long weekend with average gas prices above $4.50 a gallon, having spent an extra $20 billion at the pump in the last twelve weeks as a direct result of the Iran war. It is all this as much as anything else that might bring the conflict to some kind of a resolution relatively soon.

If you are not yet a financial planning or investment management client of Anglia Advisors and would like to explore becoming one, please feel free to reach out to arrange a complimentary no-obligation discovery call with me.

ARTICLE OF THE WEEK ..

“Evidence of a ferocious backlash against AI, especially among young people, is everywhere”. College grads just aren’t having it.

.. AND I QUOTE ..

“It’s not cost cutting; it’s replacing in some cases lower-value human capital with the financial capital and the investment capital we’re putting in.”

Bill Winters, CEO of Standard Chartered Bank, was widely slammed for this clumsy quote last week, describing the bank’s employees as “lower-value human capital”.

LAST WEEK BY THE NUMBERS:

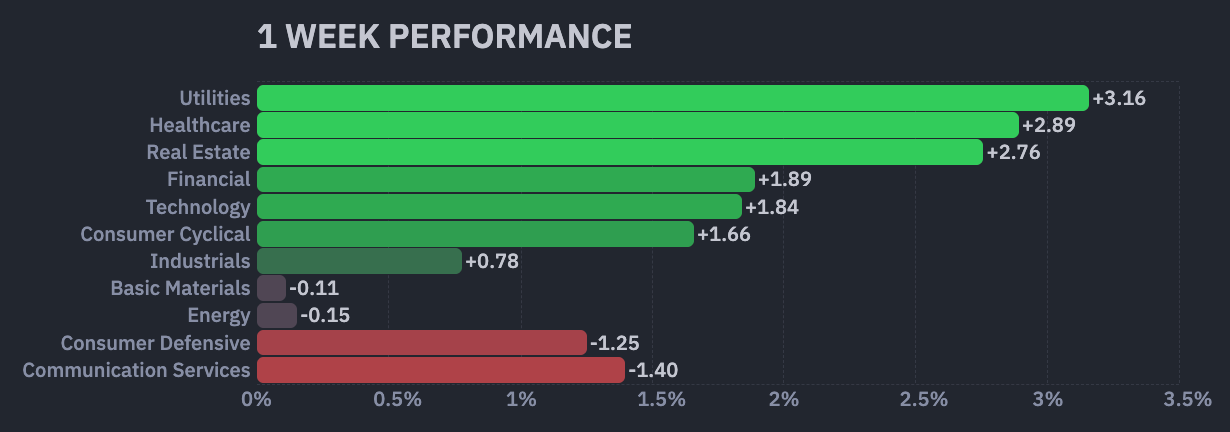

Last week’s S&P 500 market color courtesy of finviz.com

SPY, a US Large Cap ETF, tracks the S&P 500 index, made up of 500 stocks from a universe of the largest US companies. Its price rose 1.0% last week, is higher by 4.2% over the last three months and is up 5.7% so far this year.

IWM, a US Small Cap ETF, tracks the Russell 2000 index, made up of the bottom two-thirds in terms of company size of a universe of 3,000 of the largest US stocks. Its price rose 2.9% last week, is higher by 7.4% over the last three months and is up 13.2% so far this year.

VXUS, an International Non-US ETF, tracks the MSCI ACWI Ex-US index, made up of over 8,500 of the largest names from a universe of stocks issued by companies from around the world excluding the United States, in both developed and emerging markets. Its price rose 1.4% last week, is higher by 4.1% over the last three months and is up 10.1% so far this year.

INTEREST RATES:

FED FUNDS RATE * ⬌ 3.625% (unchanged from a week ago)

PRIME RATE ** ⬌ 6.75% (unchanged from a week ago)

3 MONTH TREASURY ⬇︎ 3.68% (3.69% a week ago)

2 YEAR TREASURY ⬆︎ 4.13% (4.09% a week ago)

5 YEAR TREASURY ⬆︎ 4.27% (4.26% a week ago)

10 YEAR TREASURY *** ⬇︎ 4.56% (4.59% a week ago)

20 YEAR TREASURY ⬇︎ 5.06% (5.14% a week ago)

30 YEAR TREASURY ⬇︎ 5.07% (5.12% a week ago)

Data courtesy of the Federal Reserve and the Department of the Treasury as of Friday’s market close.

* Decided upon by the Federal Reserve Open Market Committee at periodic meetings 8x a year. Used as a basis for overnight interbank loans and for determining high yield savings interest rates.

** Wall Street Journal Prime Rate as of Friday’s close. Tending to move in lockstep with the Fed Funds Rate, this measure is used as a basis for determining certain consumer loan interest rates such as credit cards, auto loans, personal loans, home equity loans/lines of credit and securities-based lending.

*** Used as a basis for determining mortgage interest rates.

AVERAGE 30-YEAR FIXED MORTGAGE RATE:

⬆︎ 6.51%

One week ago: 6.36%, one month ago: 6.24%, one year ago: 6.86%

Data courtesy of the Federal Reserve Bank of St. Louis.

INTEREST RATE EXPECTATIONS:

Where will the Fed Funds interest rate be after the next rate-setting meeting on June 17th?

0.25% higher than now .. ⬌ 0% probability (0% a week ago)

Unchanged from now .. ⬌ 99% probability (99% a week ago)

0.25% lower than now .. ⬌ 1% probability (1% a week ago)

With five more rate-setting meetings this year, what is the most commonly-expected number of remaining Fed Funds interest rate changes in 2026?

One raise (Changed from “No changes” a week ago)

Data courtesy of the CME FedWatch Tool and is derived from futures market pricing as of Friday’s market close based on the current Fed Funds interest rate of 3.625%.

PERCENT OF S&P 500 STOCKS ABOVE THEIR OWN 200-DAY MOVING AVERAGE:

⬆︎ 57%

One week ago: 51%, one month ago: 50%, one year ago: 42%

Data courtesy of barchart.com as of Friday’s market close.

This widely-used technical measure of market breadth is considered to be a very robust indicator of the overall health of the S&P 500 index.

A high percentage (above 70%) generally suggests broad market strength and a bullish trend, while a low percentage (below 30%) may indicate market weakness and a bearish trend.

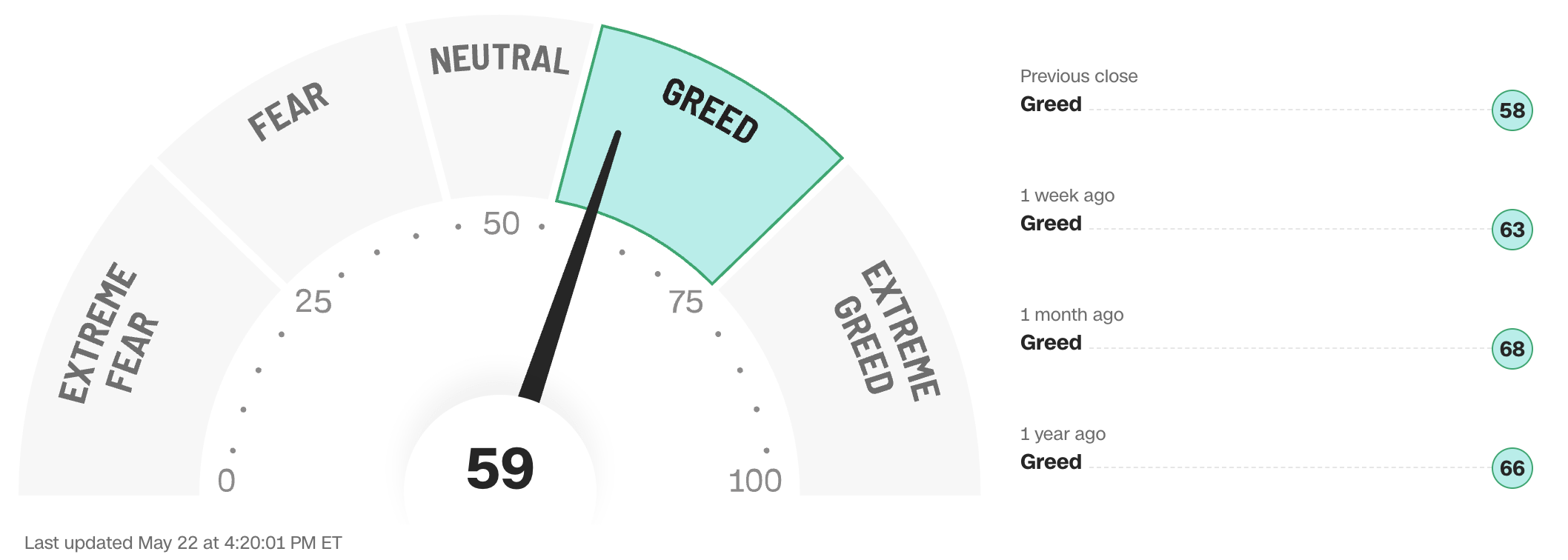

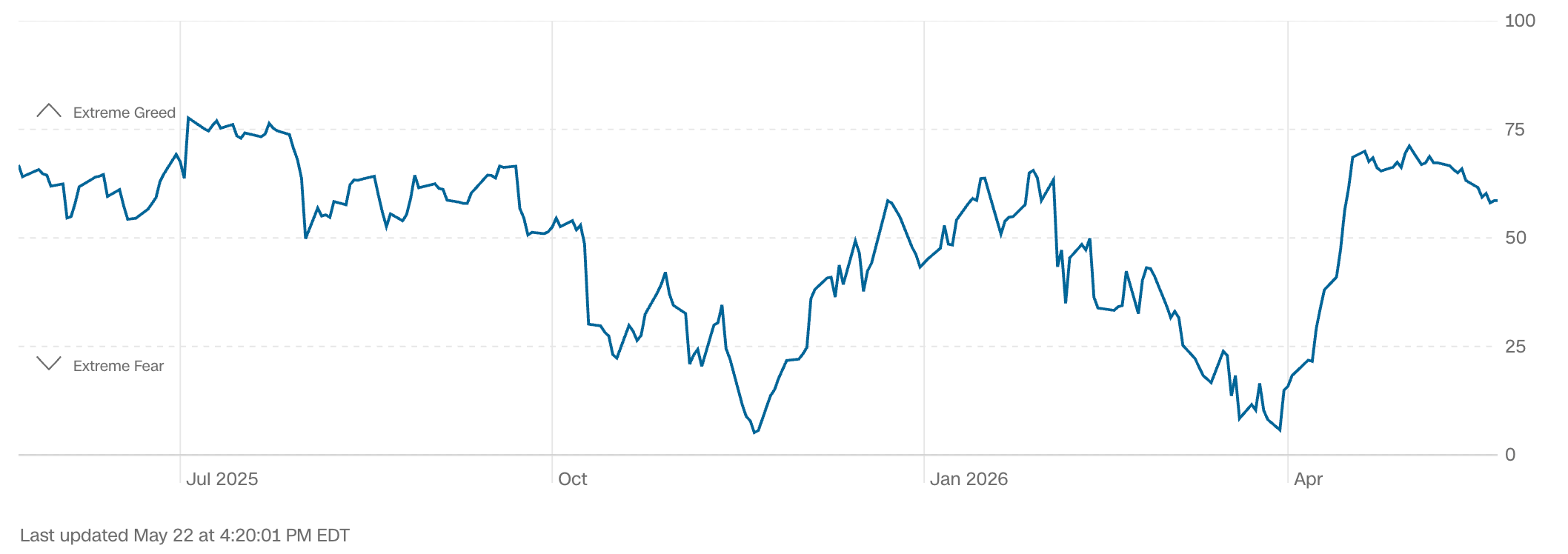

FEAR & GREED INDEX:

“Be fearful when others are greedy and be greedy when others are fearful.” Warren Buffett.

Data courtesy of CNN Business as of Friday’s market close.

The Fear & Greed Index from CNN Business can be used as an attempt to gauge whether or not stocks are fairly priced and to determine the mood of the market. It is a compilation of seven of the most important indicators that measure different aspects of stock market behavior. They are: market momentum, stock price strength, stock price breadth, put and call option ratio, junk bond demand, market volatility and safe haven demand.

Extreme Fear readings can lead to potential opportunities as investors may have driven prices “too low” from a possibly excessive risk-off negative sentiment.

Extreme Greed readings can be associated with possibly too-frothy prices and a sense of “FOMO” with investors chasing rallies in an excessively risk-on environment . This overcrowded positioning leaves the market potentially vulnerable to a sharp downward reversal at some point.

Anglia Advisors has updated its Privacy Policy. You can view the latest version here.

WWW.ANGLIAADVISORS.COM | SIMON@ANGLIAADVISORS.COM | CALL OR TEXT: (646) 286 0290 | FOLLOW ANGLIA ADVISORS ON INSTAGRAM

This material represents a highly opinionated, speculative assessment of the financial market environment based on assumptions and prevailing information and data at a specific point in time and is always subject to change at any time. Although the content is believed to be correct at the time of publication, no warranty of its accuracy or completeness is ever given. It is never to be interpreted as an attempt to forecast any future events, nor does it offer any kind of guarantee whatsoever of future results, circumstances or outcomes.

The material contained herein is not necessarily complete and is also wholly insufficient to be relied upon as research or investment advice or as a sole basis for any financial determinations, including investment decisions or making any kind of consumer choices, without further consultation with Anglia Advisors or other fully-qualified Registered Investment Advisor. The user assumes the entire risk of any decisions made or actions taken based in whole or in part on any of the information provided in this or any other Anglia Advisors published content.

Under no circumstances is any Anglia Advisors’ content ever intended to constitute tax, legal or medical advice and should never be taken as such. Neither the information contained nor any opinion expressed herein constitutes a solicitation for the purchase of any security or asset class. No formal client advice may be rendered by Anglia Advisors unless and until a properly-executed client engagement agreement is in place.

Posts may contain links or references to third party websites or may post data or graphics from them for the convenience and interest of readers. While Anglia Advisors might have reason to believe in the quality of the content provided on these sites, the firm has no control over, and is not in any way responsible for, the accuracy of such content nor for the security or privacy protocols that external sites may or may not employ. By making use of such links, the user assumes, in its entirety, any kind of risk associated with accessing them or making use of any information provided therein.

Those associated with Anglia Advisors, including clients with managed or advised investments, may maintain positions in securities and/or asset classes mentioned in this post.

If you enjoyed this post, why not share it with someone?