As anticipated, the powerful symbolism of US sovereign debt being stripped of its final AAA credit rating the previous week weighed on stocks and unnerved the bond market on Monday morning.

Trump of course deflected by blaming Biden, but the fact is that a downgrade like this results from the potential fiscal recklessness of this administration and also from foreign investors being driven to look towards their home markets rather than funding US deficits with their money.

The bond vigilantes are definitely beginning to stir. As one analyst put it; “The US government deficit isn’t a problem until the bond market decides it is.”

The day began with a toxic brew of stocks and the US Dollar selling off and interest rates shifting higher thereby pushing bond prices lower (see INTEREST RATES below). But stock indexes staged a comeback, mostly spurred by BTFD activity and inched back into the green by early afternoon and stayed just about positive through the close.

Attention began to switch on Tuesday from the Moody’s downgrade to the painfully slow progress of the massive tax and spending bill lumbering through Congress. Stocks took a big step back from their recent run up, closing lower (dragged down mainly by Tech/AI) and snapping a six-day winning streak for the S&P 500. The Healthcare sector was hurt again by the astounding decision by the newly-conspiracy theory-inspired Federal Drug Administration (FDA) that it was going to restrict Americans’ access to new COVID vaccines.

Interest rates surged higher on Wednesday and into a couple of “semi-danger zones” with the 30 year Treasury rate now above 5.00% and the 10 year (from which mortgage rates pivot) over 4.50%. Target badly missed on earnings, citing shopper pullback and the retailer slashed its forward guidance in the face of tariffs.

Stocks dumped and the US Dollar fell to its lowest level in two years, confirming another dose of the toxic brew. The more the stock and bond markets learn about how this tax and spending bill is shaping up with a lot of new spending in it but only a highly uncertain and ever-declining amount of spending cuts, the more their worries are shifting from it not being passed to the possible consequences of it actually going through.

Accordingly, when the House passed the deficit-expanding bill on Thursday morning and sent it to the Senate for what will likely be a big edit, interest rates jumped again, propelling the 30 year Treasury rate to levels not seen since 2007. While glancing nervously at the bond market, stocks just about managed to remain steady, closing the session unchanged.

Friday marked the half-way point in the tariff pause which is scheduled to end on July 9th. Interest rates pulled back, with the bond market somewhat comforted by the Supreme Court reiterating that the president cannot fire Fed chairman Powell.

But Trump seemed to wake up in a belligerent mood, tossing out a barrage of pre-market social media threats aimed at Apple, Samsung, Harvard and the European Union.

Stocks took an “uh-oh, here we go again” attitude and tumbled at the open. The indexes made a half-hearted attempt at a rally later on but still finished down on the session to end what was a rather miserable week.

It’s important to recognize that financial markets are always forward-looking. As stock prices decline, market professionals look for a “stop-getting-worse” moment to start to accumulate rather than waiting for some kind of actual all-clear, which is when most retail investors start to nibble, by which time it’s too late to catch the wave.

Staying invested, steadily buying low-cost diversified ETFs and not trying to pick spots is the only rational course of action for long term non-professional investors. The timeline varies, but the stock market has never once failed to reward patience and long term consistent buying.

Attention New York and Brooklyn readers:

I will be part of an in-person panel speaking in Brooklyn on the evening of June 2nd called “Get Your Act Together”, talking about protecting the value of your assets, navigating family dynamics and legacy considerations as you or your parents age.

I’d love to see you there! RSVP at the link above.

If you are not yet a client of Anglia Advisors and would like to explore becoming one, please feel free to reach out to arrange a complimentary no-obligation discovery call with me.

ARTICLE OF THE WEEK ..

Bye-bye to the penny. But will it actually save money?

.. AND I QUOTE ..

“If you imagine yourself more powerful than Mr. Market, take just him on directly and see what happens. Imagine yourself as smarter, more powerful, able to direct events with greater alacrity and influence? ..You’ll quickly learn who is the market’s bitch.”

Barry Ritholtz, author and founder/chief investment officer of Ritholtz Wealth Management

LAST WEEK BY THE NUMBERS:

Last week’s market color courtesy of finviz.com

Last week’s best performing US sector: Consumer Defensive (two biggest holdings: Costco, Walmart) ⬇︎ 0.3% for the week

Last week’s worst performing US sector: Energy (two biggest holdings: Exxon-Mobil, Chevron) for the second week in a row ⬇︎ 4.1% for the week

SPY, the S&P 500 Large Cap ETF, tracks the S&P 500 index, made up of 500 stocks from a universe of the largest U.S. companies. Its price fell 2.5% last week, is down 1.2% so far this year and ended the week 5.6% below its all-time record closing high (02/19/2025).

IWM, the Russell 2000 Small Cap ETF, tracks the Russell 2000 index, made up of the bottom two-thirds in terms of company size of a universe of 3,000 of the largest U.S. stocks. Its price fell 3.6% last week, is down 8.4% so far this year and ended the week 16.5% below its all-time record closing high (11/08/2021).

INTEREST RATES:

FED FUNDS * ⬌ 4.33% (unchanged)

PRIME RATE ** ⬌ 7.50% (unchanged)

3 MONTH TREASURY ⬇︎ 4.36% (4.37% a week ago)

2 YEAR TREASURY ⬆︎ 4.00% (3.98% a week ago)

5 YEAR TREASURY ⬆︎ 4.08% (4.06% a week ago)

10 YEAR TREASURY *** ⬆︎ 4.51% (4.43% a week ago)

20 YEAR TREASURY ⬆︎ 5.03% (4.92% a week ago)

30 YEAR TREASURY ⬆︎ 5.04% (4.89% a week ago)

Treasury data courtesy of ustreasuryyieldcurve.com as of the market close on Friday.

* Decided upon by the Federal Reserve. Used as a basis for interbank loans and for determining high yield savings rates.

** Wall Street Journal Prime rate. Used as a basis for determining many consumer loan rates such as credit cards, personal loans, home equity, securities-based lending and auto loans.

*** Used as a basis for determining mortgage rates.

AVERAGE 30-YEAR FIXED MORTGAGE RATE:

⬆︎ 6.86%

One week ago: 6.81%, one month ago: 6.82%, one year ago: 6.94%

Data courtesy of: FRED Economic Data, St. Louis Fed as of last Thursday.

FEDWATCH INTEREST RATE TOOL:

Where will the Fed Funds interest rate be after the next rate-setting meeting on June 18th?

Unchanged from now .. ⬆︎ 96% probability (91% a week ago)

0.25% lower than now .. ⬇︎ 4% probability (9% a week ago)

What is the most commonly-expected number of remaining 0.25% Fed Funds interest rate cuts in 2025?

⬌ 2 (unchanged from a week ago)

All data based on the Fed Funds interest rate (currently 4.33%). Calculated from Federal Funds futures prices as of the market close on Friday. Data courtesy of CME FedWatch Tool.

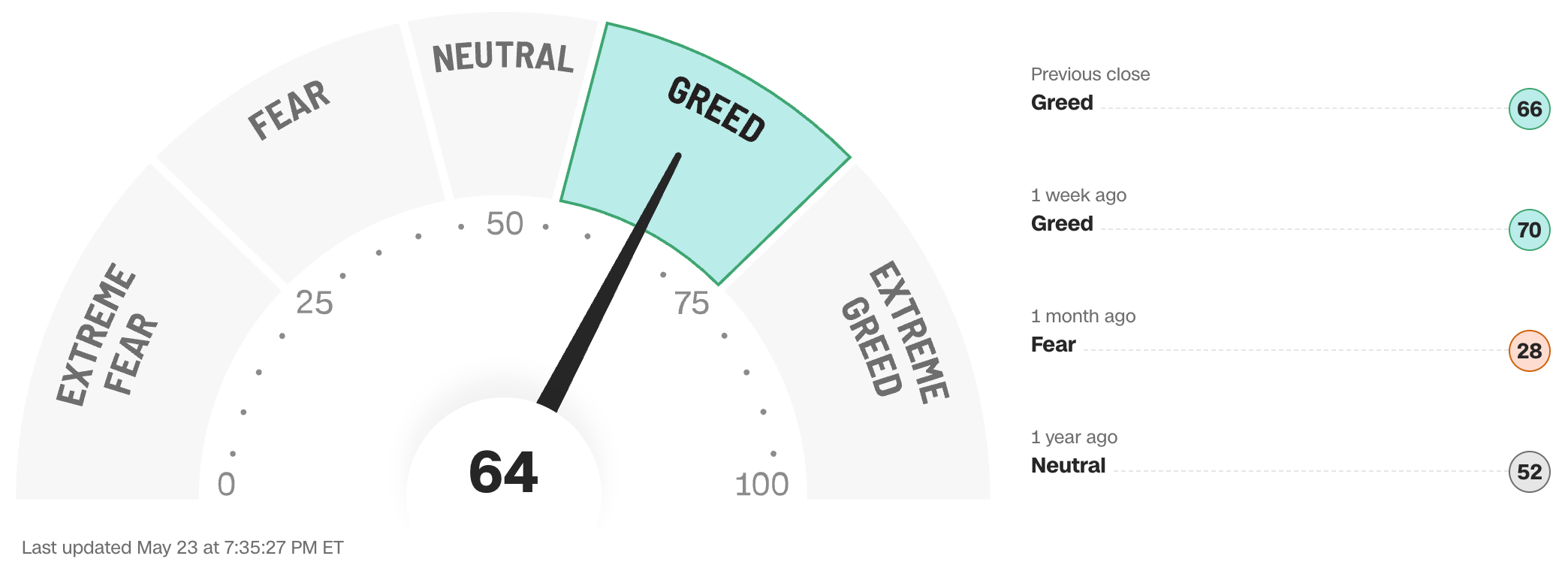

FEAR & GREED INDEX:

“Be fearful when others are greedy and be greedy when others are fearful.” Warren Buffet.

The Fear & Greed Index from CNN Business can be used as an attempt to gauge whether or not stocks are fairly priced and to determine the mood of the market. It is a compilation of seven of the most important indicators that measure different aspects of stock market behavior. They are: market momentum, stock price strength, stock price breadth, put and call option ratio, junk bond demand, market volatility and safe haven demand.

Extreme Fear readings can lead to potential opportunities as investors may have driven prices “too low” from a possibly excessive risk-off negative sentiment.

Extreme Greed readings can be associated with possibly too-frothy prices and a sense of “FOMO” with investors chasing rallies in an excessively risk-on environment . This overcrowded positioning leaves the market potentially vulnerable to a sharp downward reversal at some point.

A “sweet spot” is considered to be in the lower-to-mid “Greed” zone.

Data courtesy of CNN Business as of Friday’s market close.

WWW.ANGLIAADVISORS.COM | SIMON@ANGLIAADVISORS.COM | CALL OR TEXT: (646) 286 0290 | FOLLOW ANGLIA ADVISORS ON INSTAGRAM

This material represents a highly opinionated assessment of the financial market environment based on assumptions and prevailing information and data at a specific point in time and is always subject to change at any time. Although the content is believed to be correct at the time of publication, no warranty of its accuracy or completeness is given. It is never to be interpreted as an attempt to forecast any future events, nor does it offer any kind of guarantee of any future results, circumstances or outcomes.

The material contained herein is not necessarily complete and is also wholly insufficient to be exclusively relied upon as research or investment advice or as a sole basis for any financial decisions, including investment decisions or making any kind of consumer choices, without further consultation with Anglia Advisors or other qualified Registered Investment Advisor. The user assumes the entire risk of any decisions made or actions taken based in whole or in part on any of the information provided in this or any other Anglia Advisors published content.

Under no circumstances is any of Anglia Advisors’ content ever intended to constitute tax, legal or medical advice and should never be taken as such. Neither the information contained or any opinion expressed herein constitutes a solicitation for the purchase of any security or asset class. No client advice may be rendered by Anglia Advisors unless and until a properly-executed Client Engagement Agreement is in place.

Posts may contain links or references to third party websites or may post data or graphics from them for the convenience and interest of readers. While Anglia Advisors might have reason to believe in the quality of the content provided on these sites, the firm has no control over, and is not in any way responsible for, the accuracy of such content nor for the security or privacy protocols that external sites may or may not employ. By making use of such links, the user assumes, in its entirety, any kind of risk associated with accessing them or making use of any information provided therein.

Those associated with Anglia Advisors, including clients with managed or advised investments, may maintain positions in securities and/or asset classes mentioned in this post.

If you enjoyed this post, why not share it with someone or encourage them to subscribe themselves?