According to Wall Street’s categorization rules, the S&P 500 index exited bear market territory on Thursday when it closed up more than 20% from its lows from October of last year after spending 248 days there - the longest bear stretch since 1948. However, it still ended the week 10% below its all-time high from January 3rd 2022.

While there’s absolutely nothing in the rules that says we can’t roll over into another new bear market right away, this one we’ve just been through is technically over. For what that’s worth.

With shadow of a debt ceiling crisis now gone and the regional banking catastrophe simply not happening, the path to additional positive surprises is getting narrower and, because so much good news has been priced in already, even a near-perfect best case scenario will likely produce only a modest further rally. Any kind of disappointment, on the other hand, could easily open up a quick 5-10% downward “air pocket” in stock prices, particularly for those assets that have done so well in recent weeks.

Having said that, there’s a definite sense that FOMO is starting to grip those who are under-invested or who’ve been waiting around on the sidelines as the biggest influence on their decision-making shifts from fear at the beginning of the year to extreme greed now (see this report’s new weekly feature; the FEAR & GREED INDEX below).

There’s a growing perception that it might be a bigger risk to be out of the stock market rather than in it. That’s the very definition of the “pain trade”, professional money managers buying stocks not because it’s a rational considered choice, but because they feel pressured to do so by a growing fear of missing an opportunity. Indeed, the head of Citigroup’s US Equity Trading Strategy acknowledged this sentiment just last week when he said on Bloomberg TV, “We are reluctantly staying in the tech trade.”

This causes them to frantically chase stocks higher, driving the indexes up. Until one day they stop. Which could then leave the market a bit like Wile E. Coyote when he suddenly stops running and realizes he has just chased the Roadrunner over the edge of a cliff.

We’re seeing a shift in sector leadership as markets embrace hope for a more broadly robust economy and grow in belief in the soft landing and I would expect the performance gap between the recently-ripping tech and tech-adjacent sectors and the so-far-lagging, more value-oriented consumer sectors to continue to narrow in the short term, at least.

A greater-than-expected rise in weekly unemployment claims on Thursday increased the bets that the Fed will pause raising interest rates this week. It’s important to note that the Fed being “on hold” should not be confused with “job done”. There has been a subtle shift in language from “pause” to “skip” when discussing the Fed not hiking on Wednesday, which is trying to communicate that a pause isn’t a permanent on-hold and it certainly doesn’t mean that rate cuts are imminent.

Tuesday's release of the Consumer Price Index (CPI) measure of retail inflation for May and Wednesday morning’s release of the Producer Price Index (PPI) measure of wholesale inflation experienced by manufacturers will both be major influences on the Fed who will announce their interest rate decision later on Wednesday (at 2pm ET). While red-hot inflation could spell trouble for those betting on a June pause followed swiftly by a rate cut, definitive signs of a cooldown could have the capability to keep the upward momentum in stock prices going for a while longer.

Interest rates across the old British empire continue to move higher as central banks in Australia and Canada both surprised markets by hiking a quarter of a point last week, citing still-elevated inflation. Particularly in the case of Canada, this rate increase followed a lengthy pause. Blueprint for the Fed?

As can be seen in the FEDWATCH INTEREST RATE PREDICTION TOOL below, many stock market participants still believe that the next change in US interest rates after the assumed pause/skip this time around will be a downward one. The Bank of Canada just reminded us that this may well not be the case.

The World Bank (WB) released updated growth forecasts on Wednesday. The revisions were to the upside with the WB’s anticipated US growth rate for 2023 being raised from 0.5% in January to 1.1%. Global growth expectations also increased from 1.7% in January to 2.1%, with the bank citing “greater-than-expected resilience in major world economies.”

Goldman Sachs analysts came out last week and announced; “We have cut our judgmental probability that the US economy will enter a recession in the next twelve months back to 25%, undoing our upward revision to 35% shortly after the Silicon Valley Bank failure ..“

While a Wall Street analyst’s measure of success is generally a matter of being just slightly less wrong than a competitor, this shift is symptomatic of the mood of many investors that the economic landing may well be softer than was feared coming into 2023. And if there is going to be a meaningful recession, it will be the most well-telegraphed and anticipated one in history as little else has been on investors’ minds for over a year now.

Oh, and Wall Street will simply yawn at the arrival of yet another Trump legal circus just like it has done historically.

OTHER NEWS ..

Regulators at the SEC have had crypto in their sights for a while. Last week they pulled the trigger ..

After months of teasing, the Securities and Exchange Commission (SEC) finally took the gloves off last week when it comes to investor protection in the world of crypto. On Tuesday the SEC sued Coinbase (COIN), alleging that the US’s largest crypto platform violated rules that require it to be held accountable and to register as an exchange and be overseen by the federal agency - predictably crashing the stock. The SEC filed the lawsuit in Manhattan federal court. The SEC alleged that Coinbase traded at least 13 crypto assets that are really unregistered securities (see EXPLAINER: FINANCIAL TERM OF THE WEEK, below) and should have been registered with regulators before they were issued and also that there was illicit activity in crypto-staking. Registration typically involves giving investors financial statements and detailed risk disclosures that are reviewed by regulators.

The case came just 24 hours after the regulator’s 136-page enforcement action against Binance and its founder ChangPeng Zhao alleging that the world’s largest crypto exchange is not only operating an illegal trading platform in the US but (unlike on the list of the Coinbase charges) also improperly misused (pretty much legal-speak for “stole”) customers’ funds, directing them into other entities owned by CZ in a manner that has echoes of the fraudulent activity allegedly carried out by Sam Bankman-Fried at FTX (SBF is facing a criminal trial and potentially decades in jail if convicted). Later in the week, some highly-incriminating messages from CZ were released by the SEC.

Kicking laser-eyed crypto bros while they were down, SEC chairman Gary Gensler, a former MIT blockchain professor who actually really knows his crypto shit, then came out and said on CNBC that cryptocurrencies are essentially unnecessary in today’s world; “Look, we don’t need more digital currency,” he said “We already have digital currency. It’s called the US dollar. It’s called the euro or it’s called the yen; they’re all digital right now. We already have digital investments.”

Matt Levine of Bloomberg put it this way .. “The SEC, I think, learned three lessons: 1) Almost all crypto tokens are securities, 2) Winning cases against crypto projects for doing illegal securities offerings is pretty easy, 3) Especially when they are also frauds”.

John Reed Stark, former SEC enforcement attorney, even went as far as to say in response to last week’s enforcement actions; “I think anyone who has crypto on any exchange should take it off of that exchange immediately. Period, end of story.”

Oh Elon! ..

Fresh from watching his Space X rocket exploding right after launch, recently learning from Fidelity that Twitter is actually worth only about a third of what he paid for it and spectacularly bungling the launch of Ron DeSantis’ presidential campaign, Elon Musk has even more serious problems coming his way. He is now being accused of insider trading in a class action law suit by multiple investors who say he manipulated the cryptocurrency Dogecoin, costing them billions of dollars.

In a filing in Manhattan federal court, it was claimed by investors that Musk used Twitter posts, highly-paid online influencers, his awkward 2021 appearance on NBC's "Saturday Night Live" and other "publicity stunts" to trade manipulatively and make money at their expense through several Dogecoin wallets controlled by him or by Tesla. The accusation is that Musk deliberately and strategically drove up Dogecoin's price more than 36,000% in a scheming manner over the course of two years only to then let it crash, enriching himself along the way.

They said that this strategy included, in April of this year, Musk briefly replacing Twitter's blue bird logo with that of Dogecoin's Shiba Inu dog, which led to a swift 30% spike in Dogecoin's price into which Musk then proceeded to sell $124 million-worth of the cryptocurrency.

A "deliberate course of carnival barking, market manipulation and insider trading" enabled Musk to defraud investors while enriching and promoting himself and his companies, according to the filing.

Watch this space, it could get spicy.

UNDER THE HOOD ..

Technical analysis advocates will tell you that the market has a memory. The last time the index got up to 4300 in August of last year, we ran out of buyers and it quickly sank. It closed at 4298 on Friday, so it will be interesting to see what happens from here.

While Buying Power vs Selling Pressure and breadth dynamics have improved nicely over the last couple of weeks, there’s still a slightly disconcerting pattern of trading volume expanding on the down days and falling on the up days. And a fundamental technical rationale for the S&P 500's 20% rally since October is still kind of missing when you compare that data with that of pretty much every other major market bottom in history.

To technical analysts, if October 2022 was indeed the final turning point, then it seems too good to be true and that bothers them. Others may point out that COVID and the Federal Reserve’s response has broken almost all economic and financial charts, rules and precedents and maybe this is just another example of this and the word “unprecedented” has very little power any more.

Last week was particularly notable for improved participation rates with recently-lagging Mid and Small Cap stocks handsomely outperforming their Large Cap cousins.

Anglia Advisors clients are welcome to reach out to me to discuss market conditions further.

THIS WEEK’S UPCOMING CALENDAR ..

This week is a huge one on the economic data and policy fronts. Investors will contend with major inflation data and central bank meetings.

The Federal Reserve's monetary policy committee will announce its latest interest rate decision on Wednesday afternoon. Markets are overwhelmingly pricing in no change. The European Central Bank is widely expected to raise its target interest rate by a quarter of a point on Thursday.

Before that Fed decision, we will get the latest Consumer Price Index (CPI) measure of retail inflation for May and the Producer Price Index (PPI) measure of wholesale inflation experienced by manufacturers. The consensus estimates are for increases of 4.2% and 1.5%, respectively.

Other economic data out next week includes Retail Sales data for May and the latest Consumer Sentiment Index.

Q1 2023 earnings reports will come from Oracle, Adobe, Kroger and Lennar. Home Depot will host an investor day.

AVERAGE 30-YEAR FIXED RATE MORTGAGE ..

6.71%

(one week ago: 6.79%, one month ago: 6.35%, one year ago: 5.23%)

Data courtesy of: FRED Economic Data, St. Louis Fed as of Thursday of last week.

US INVESTOR SENTIMENT (outlook for the upcoming 6 months) ..

↑Bullish: 45% (29% a week ago)

↔ Neutral: 31% (34% a week ago)

↓Bearish: 24% (37% a week ago)

Net Bull-Bear spread: ↑Bullish by 21 (Bearish by 8 a week ago)

(Sentiment readings flipped from majority bearish to majority bullish last week)

Data courtesy of: American Association of Individual Investors (AAII).

For context: Long term averages: Bullish: 38% — Neutral: 32% — Bearish: 30% — Net Bull-Bear spread: Bullish by 8

Weekly sentiment survey participants are usually polled on Tuesdays and/or Wednesdays.

FEAR & GREED INDEX ..

The Fear & Greed Index from CNN Business is a way to gauge whether stocks are fairly priced or not. It is a compilation of seven different indicators that measure some aspect of stock market behavior. They are market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility and safe haven demand.

The index can be used as an attempt to determine the mood of the market. Extreme Fear readings can lead to potential opportunities as investors may have driven prices “too low” from a possibly excessive risk-off negative sentiment. Extreme Greed readings can be associated with a sense of “FOMO” and investors chasing rallies in an excessively risk-on environment, possibly leaving the market vulnerable to a sharp downward correction at some point. It is important to note that either of these extreme conditions may persist for considerable periods of time.

Data courtesy of CNN Business.

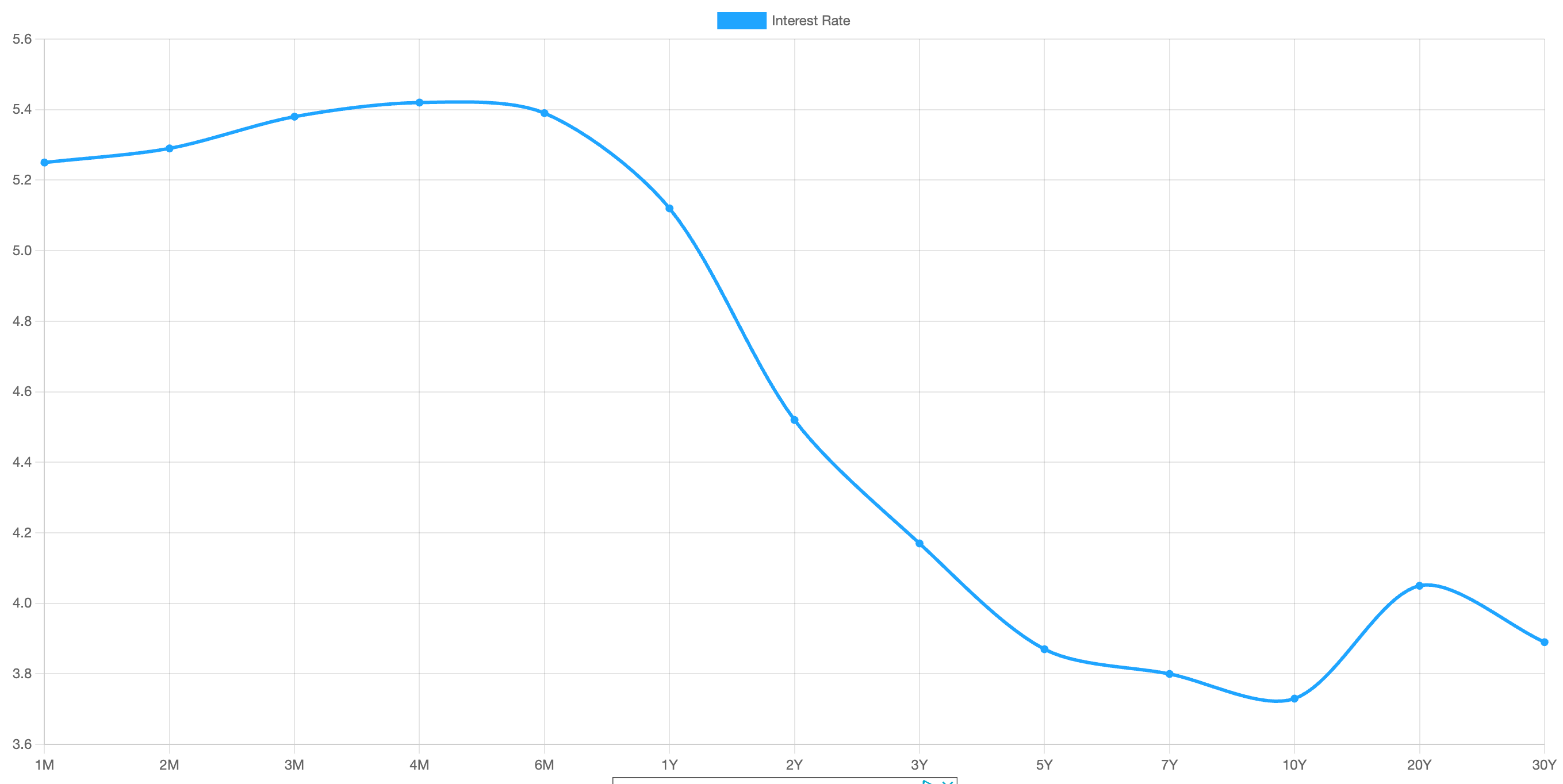

US TREASURY INTEREST RATE YIELD CURVE ..

The interest rate yield curve remains “inverted” (i.e. most shorter term interest rates are higher than longer term ones) with the highest rate (5.42%) being paid currently for the 4-month duration and the lowest rate (3.73%) for the 10-year.

The closely-watched and most commonly-used comparative measure of the spread between the 2-year and the 10-year last week fell from 0.81% to 0.79%, indicating an overall flattening of the inversion of the curve during the last five days.

Historically, an inverted yield curve has been regarded as a leading indicator of an impending recession, with shorter term risk deemed to be unusually higher than longer term.

The curve has been inverted since July 2022 based on the 2 year vs. 10 year spread.

Data courtesy of ustreasuryyieldcurve.com as of Friday.

FEDWATCH INTEREST RATE PREDICTION TOOL ..

Where will interest rates (Fed Funds rate, currently 5.125%) be at the end of 2023?

↑ Higher than now .. 30% probability

(one week ago: 21%, one month ago: 0%)

↔ Unchanged from now .. 38% probability

(one week ago: 36%, one month ago: 1%)

↓ Lower than now .. 32% probability

(one week ago: 43%, one month ago: 99%)

What are the latest market expectations for what the Fed will announce re: interest rate changes (Fed Funds rate, currently 5.125%) on June 14th after its next meeting?

↑ 0.25% increase .. 29% probability

(one week ago: 28%, one month ago: 21%)

↔ No change .. 71% probability

(one week ago: 72%, one month ago: 79%)

↓ 0.25% cut .. 0% probability

(one week ago: 0%, one month ago: 0%)

Data courtesy of CME FedWatch Tool. Calculated from Federal Funds futures prices as of Friday.

LAST WEEK BY THE NUMBERS ..

Last week’s market color courtesy of finviz.com:

- Last week’s best performing US sector: Consumer Cyclical (two biggest holdings: Amazon, Tesla) - up 2.7% for the week.

- Last week’s worst performing US sector: Consumer Defensive (two biggest holdings: Proctor and Gamble, Pepsico) for the third week in a row - down 0.7% for the week.

- The proprietary Lowry's measure for US Market Buying Power is currently at 158 and rose by 9 points last week and that of US Market Selling Pressure is now at 137 and fell by 16 points over the course of the week.

- SPY, the S&P 500 ETF, remains above its 50-day and 90-day moving averages and above its long term trend line with a RSI of 67**. SPY ended the week 10.0% below its all-time high (01/03/2022).

- QQQ, the NASDAQ-100 ETF, remains above its 50-day and 90-day moving averages and above its long term trend line with a RSI of 70**. QQQ ended the week 12.2% below its all-time high (11/19/2021).

** RSI (Relative Strength Index) above 70: technically over-bought, RSI below 30: technically over-sold

- VIX, the commonly-accepted measure of expected upcoming stock market risk and volatility (often referred to as the “fear index”), implied by S&P 500 index option trading, ended the week 0.8 points lower at 13.8. It remains below its 50-day and 90-day moving averages and below its long term trend line.

ARTICLE OF THE WEEK ..

Is right now the absolute worst time ever to buy a house? Ben Carlson runs some numbers.

EXPLAINER: FINANCIAL TERM OF THE WEEK ..

A weekly feature using information found on Investopedia to try to help explain Wall Street gobbledygook (may be edited at times for clarity).

Before securities—like stocks, bonds, and notes—can be offered for sale to the public, they first must be registered with the Securities and Exchange Commission (SEC). Any stock that does not have an effective registration statement on file with the SEC is considered to be unregistered.

To sell or attempt to sell a financial security before it is registered is considered a felony.

However, certain exemptions apply. For example, a privately-owned corporation may issue shares of stock to its executives and board members. However, the new stockholders must notify the SEC before selling the stock to anyone else.

In addition, companies can raise capital by soliciting investments from individuals outside the company who are considered to be "qualified investors." The SEC defines a qualified investor as someone who has a net worth of at least one million dollars or an annual income in excess of $200,000.

Individuals who meet "qualified investor" status can sometimes become victims of unregistered securities scams that are advertised as "private offerings." In April 2019, Investment News published an article called "Sales of Unregistered Securities Are a Growing Problem That's Harming Every Investor—and the Industry."5

Bruce Kelly of Investment News uses the example of Castleberry Financial Services Group. The company managed to raise $3.6 million from investors by offering what they called an "alternative investment fund" that promised up to a 12.2% annual yield.

However, an investigation by the Securities and Exchange Commission (SEC) revealed that some of the money they'd raised had been used to pay the personal expenses of the firm's principals. Funds were also transferred to family members and other businesses that the principals controlled. The SEC eventually took the company to court and shut them down.

However, Kelly points out that this kind of scheme—where private, unregistered securities are sold to wealthy investors and institutions—is not unusual and is, in fact, actually rampant in the industry:

What’s growing alongside this legitimate, if risky, market is a seedy side of the financial industry. Investment funds promising above-market returns that employ networks of brokers, former brokers, insurance agents or others lurking on the fringes of the industry to sell their investments are taking advantage of unsuspecting investors.

The marketplace for unregistered securities has grown, partially because private securities can be sold over the internet and companies can solicit clients via social media. This results in unregistered, private securities being sold to investors who do not meet the SEC's criteria for "qualified investors." And according to Kelly, this is damaging the reputation of the financial advice industry.

The SEC and the Financial Industry Regulatory Authority (FINRA) are working on increasing oversight for finance professionals who sell private, unregistered securities.

WWW.ANGLIAADVISORS.COM | SIMON@ANGLIAADVISORS.COM | CALL OR TEXT: (929) 677 6774 | FOLLOW ANGLIA ADVISORS ON INSTAGRAM

This material represents a highly opinionated assessment of the financial market environment based on assumptions and prevailing data at a specific point in time and is always subject to change at any time. No warranty of its accuracy or completeness is given. It is never to be interpreted as an attempt to forecast any future events, nor does it offer any kind of guarantee of any future results, circumstances or outcomes.

The material contained herein is not necessarily complete and is wholly insufficient to be exclusively relied upon as research or investment advice or as a sole basis for any kind of investment decision or action. The user assumes the entire risk of any decisions made or actions taken based on the information provided in this or any Anglia Advisors communication of any kind. Under no circumstances is any of Anglia Advisors’ content ever intended to constitute tax, legal or medical advice and should never be taken as such. Neither the information contained or any opinion expressed herein constitutes a solicitation for the purchase of any security or asset class.

Posts may contain links or references to third party websites for the convenience and interest of readers. While Anglia Advisors may have reason to believe in the quality of the content provided on these sites, the firm has no control over, and is not in any way responsible for, the accuracy of such content nor for the security or privacy protocols that external sites may or may not employ. By making use of such links, the user assumes, in its entirety, any kind of risk associated with accessing them or making use of any information provided therein.

Clients of, and those associated with, Anglia Advisors may maintain positions in securities and asset classes mentioned in this post.

If you enjoyed this post, why not share it with someone or encourage them to subscribe themselves?