After the rapidly spiraling events in Syria over the weekend, attention was temporarily refocused on geopolitics and the potential tinderbox that is the Middle East region, where the chess pieces were being moved around following the abrupt disintegration of the Assad regime as everyone tried to work out who are the “goodies” and who are the “baddies” in this story. Both the U.S. and Israel immediately carried out self-interested attacks on Syrian soil.

Stocks dipped at the open on Monday on low-key, pretty indifferent trading and continued to drift aimlessly lower across the board as the day went on, ahead of Wednesday and Thursday’s inflation reports, the last major data to be released before the Fed’s next interest rate-setting meeting on December 18th.

Tuesday saw something of a recovery at the outset but traders began to sell Oracle stock after its earnings report failed to meet elevated expectations and the effect rippled out enveloping Dell, Hewlett Packard and other tech names that have been propping up market advances lately - with the day’s moves accentuated by the continued low volume environment. The indexes all finished lower again.

When it came out pre-market on Wednesday, the Consumer Price Index (CPI) measure of retail inflation proved to be rather sticky, rising to a +2.7% annualized rate, a larger increase than the +2.6% of the prior month. This was, however, entirely as expected and stocks quickly picked up steam, relieved to have dodged a nasty surprise ahead of this week’s Fed interest rate decision and impressed by the housing/shelter component of the inflation data, which finally showed a significant drop.

Big Tech stocks very much led the way as the losses from earlier in the week were quickly erased with the NASDAQ closing above 20k for the first time ever and Apple, Alphabet/Google, Amazon, Meta/Facebook and Tesla all setting their own individual all-time record high stock prices.

Also erased were any remaining doubts that we will get a further interest rate cut of 0.25% on Wednesday (see FEDWATCH INTEREST RATE TOOL below), although the number and pace of any cuts in 2025 is becoming increasingly uncertain.

A lot happened before Trump rang the opening bell at the New York Stock Exchange on Thursday. We saw an expected quarter point rate cut from the European Central Bank (ECB), an unexpected full 1.00% hike in Brazil and the latest U.S. Producer Price Index (PPI) measure of wholesale inflation experienced by manufacturers which came in hotter than expected at +3.0% annualized, it’s highest level since February 2023.

We also got disappointing earnings and outlook from Adobe, who joined Oracle in the dog house as Wall Street swiftly crushed the stock price by almost 15% at one point.

Traders resumed their rather ho-hum attitude following Wednesday’s Big Tech party, shifting back into a mostly wait-and-see mode, this time with eyes on the upcoming Fed meeting (the forward guidance offered rather than the interest rate cut itself, which is now assumed) as well as how Trump’s cabinet nominees play out and the indexes ended the session lower.

Over two-thirds of S&P 500 stocks fell on the day and that’s the ninth day in a row that more than half the stocks in the index have moved lower - the longest such streak since 2001. Despite the deluge of record all-time highs, there is turmoil developing beneath the surface.

Friday the 13th saw Broadcom rip by 25% (building on its 60% gain already in 2024 and becoming the eighth-ever company to be valued at over a trillion dollars) after predicting a boom in demand for its AI chips and initially tech-heavy indexes moved higher as a result.

However, rising concerns that interest rate cuts in 2025 may not match the lofty expectations upon which this rally has been built (something I have been banging on about in these reports for ages now) soured sentiment somewhat and the broad stock market finished unchanged for the day.

The S&P 500 was slightly down for the week, Small Caps were down by more but the NASDAQ scored a small weekly gain.

The path to a continued rally into year-end is clear on the back of performance chasing, seasonal factors and technical momentum, but at the same time we should all be prepared for 2025 to start with some volatility around headlines from potential policy disappointment, a possibly slower pace of interest rate cuts next year, geopolitical saber-rattling and the big wild card; tariffs.

There are signs in the recent economic data that consumers are bringing forward the purchase of big-ticket items like cars to get ahead of potential tariff-related price increases. Whether Trump is just full of it when he barks about tariffs or whether he will actually follow through on all or most of his threats is becoming an increasingly important question as they obviously pose an inflation risk as well as negatively impacting earnings potential of U.S. exporters once other countries retaliate (and make no mistake, they will).

As long as growth remains solid, the Fed is cutting rates and earnings/corporate outlook are all positive, those potential problems can just be viewed as bumps along the road in a still-upward trending market.

Bottom line, the rally is justified, but it’s strongly assuming that virtually nothing bad happens in the near-term. If that assumption is proven wrong then, given the stretched valuations of U.S. stocks, the dreaded 10%+ decline trapdoor could well quickly swing open, catching everybody off guard.

OTHER NEWS ..

Ooops, Where Did My Economic Data Go?! .. US economic indicators can move global markets by trillions of dollars at a time and in a matter of milli-seconds. The agencies that collect and publish those statistics have been pleading for an extra few million, to maintain the integrity of the financial world’s most important numbers. Now they face an even tougher fight to get it, as Donald Trump heads back to Washington with a plan to slash the federal bureaucracy.

Well before Trump won reelection on a platform that hardly prioritized reliably sourced data, the Bureau of Labor Statistics and its peers in Washington were sounding the alarm that they’re increasingly starved of funds, just when it’s becoming harder and costlier to collect the information needed for some of the most critical gauges.

Solid statistics matter far beyond financial markets. The Federal Reserve stresses that its interest-rate decisions are guided by incoming economic data. Businesses rely on government-produced figures when planning new investments. National and local politicians need them at their fingertips to guide policy decisions—from tariffs on China to the best location for hospitals or housing—that shape the lives of everyday Americans.

World’s Smallest Violin Plays In Chicago .. Michael Jordan finally managed to sell his sprawling Chicago-area mansion, settling for $9.5 million. That’s a significant price cut from the original asking price of $29 million, despite the property boasting nine bedrooms, 19 bathrooms, a regulation-sized basketball court (of course) and a cigar room (also of course). He’s not the first billionaire to sell in the area for way less than he expected. Ken Griffin, CEO of Citadel, recently sold one of his Chicago condos for 53% below what he originally paid.

ARTICLE OF THE WEEK ..

Gen Z has lived through an almost unbroken chain of financial crises of one kind or another and it’s having a massive effect on their attitudes about pretty much everything which is going to affect the society they will eventually shape for the rest of us.

THIS WEEK’S UPCOMING CALENDAR ..

The Federal Reserve concludes a two-day meeting on Wednesday. Markets are fully expecting the announcement of a quarter of a percentage point cut to the federal-funds rate. The Bank of England and Bank of Japan both announce monetary-policy decisions on Thursday.

The main economic data to watch next week is the Fed’s favorite inflation measure, the Personal Consumption Expenditures (PCE) price index for November on Friday.

The highlights on the earnings calendar are Fedex, Nike, Carnival, Micron Technology, Accenture and Lennar.

LAST WEEK BY THE NUMBERS:

Last week’s market color courtesy of finviz.com

Last week’s best performing U.S. sector: Consumer Cyclical (two biggest holdings: Amazon, Tesla) for the third week in a row - up 1.2% for the week.

Last week’s worst performing U.S. sector: Materials (two biggest holdings: Linde, Sherwin Williams) for the second week in a row - down 2.9% for the week.

SPY, the S&P 500 Large Cap ETF, tracks the S&P 500 index, made up of 500 stocks from a universe of the largest U.S. companies. Its price fell 0.7% last week, is up 27.1% so far this year and ended the week 1.5% below its all-time record closing high (12/06/2024).

IWM, the Russell 2000 Small Cap ETF, tracks the Russell 2000 index, made up of the bottom two-thirds in terms of company size of a universe of 3,000 of the largest U.S. stocks. Its price fell 2.6% last week, is up 16.1% so far this year and ended the week 3.9% below its all-time record closing high (11/08/2021).

AVERAGE 30-YEAR FIXED MORTGAGE RATE:

⬇︎ 6.60%

One week ago: 6.69%, one month ago: 6.78%, one year ago: 6.96%

Data courtesy of: FRED Economic Data, St. Louis Fed as of last Thursday.

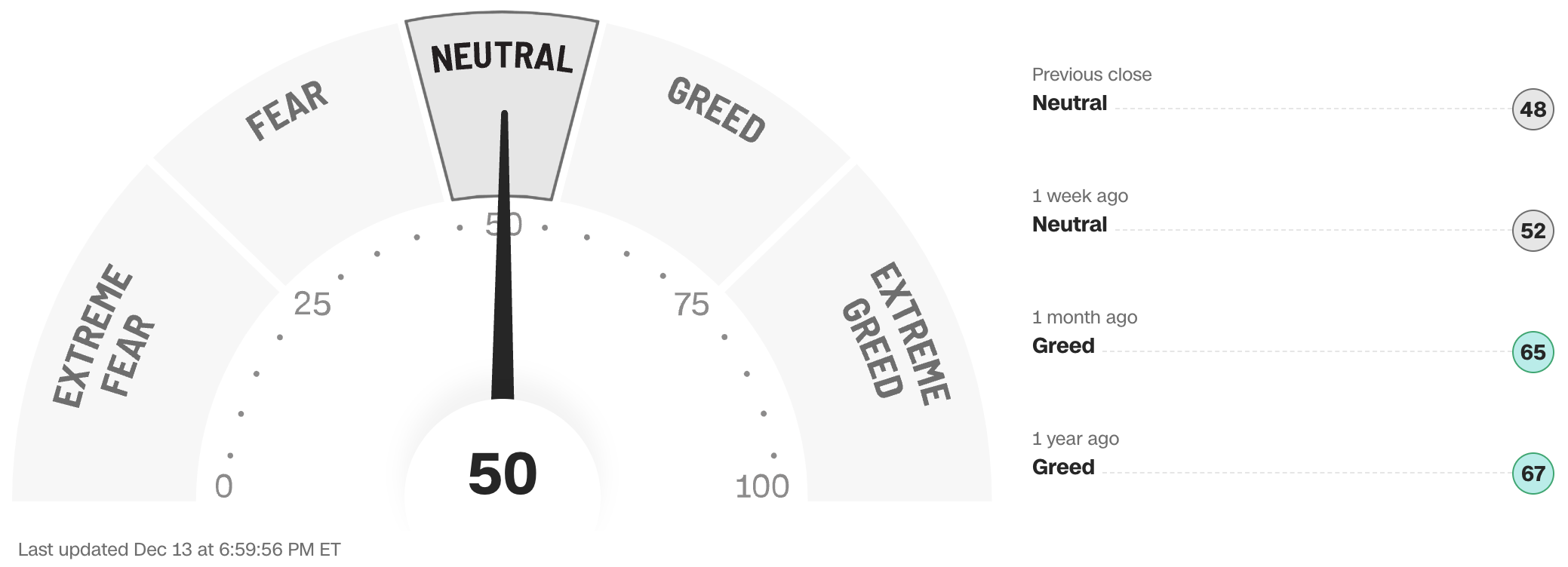

FEAR & GREED INDEX:

“Be fearful when others are greedy and be greedy when others are fearful.” Warren Buffet.

The Fear & Greed Index from CNN Business can be used as an attempt to gauge whether or not stocks are fairly priced and to determine the mood of the market. It is a compilation of seven of the most important indicators that measure different aspects of stock market behavior. They are: market momentum, stock price strength, stock price breadth, put and call option ratio, junk bond demand, market volatility and safe haven demand.

Extreme Fear readings can lead to potential opportunities as investors may have driven prices “too low” from a possibly excessive risk-off negative sentiment.

Extreme Greed readings can be associated with possibly too-frothy prices and a sense of “FOMO” with investors chasing rallies in an excessively risk-on environment . This overcrowded positioning leaves the market potentially vulnerable to a sharp downward reversal at some point.

A “sweet spot” is considered to be in the lower-to-mid “Greed” zone.

Data courtesy of CNN Business as of Friday’s market close.

FEDWATCH INTEREST RATE TOOL:

Where will interest rates be after the Fed’s next meeting on December 18th?

Higher than now .. 0% probability (0% a week ago)

Unchanged from now .. ⬇︎4% probability (14% a week ago)

0.25% lower than now .. ⬆︎96% probability (86% a week ago)

0.50% lower than now .. 0% probability (0% a week ago)

What is the most commonly expected number of 0.25% interest rate cuts from the Fed between now and the end of 2025?

3 (4 a week ago)

All data based on the Fed Funds interest rate (currently 4.625%). Calculated from Federal Funds futures prices as of the market close on Friday. Data courtesy of CME FedWatch Tool.

% OF S&P 500 STOCKS TRADING ABOVE THEIR 50-DAY MOVING AVERAGE:

⬇︎47% (235 of the S&P 500 stocks ended last week above their 50D MA and 265 were below)

One week ago: 58%, one month ago: 62%, one year ago: 89%

% OF S&P 500 STOCKS TRADING ABOVE THEIR 200-DAY MOVING AVERAGE:

⬇︎65% (323 of the S&P 500 stocks ended last week above their 200D MA and 177 were below)

One week ago: 69%, one month ago: 72%, one year ago: 72%

Closely-watched measures of market breadth and participation, providing a real-time look at how many of the S&P 500 index stocks are trending higher or lower, as defined by whether the stock price is above or below their more sensitive 50-day (short term) and less sensitive 200-day (long term) moving averages which are among the most widely-followed of all stock market technical indicators.

The higher the reading, the better the deemed health of the overall market trend, with 50% considered to be a key pivot point. Readings above 90% or below 15% are extremely rare.

WWW.ANGLIAADVISORS.COM | SIMON@ANGLIAADVISORS.COM | CALL OR TEXT: (646) 286 0290 | FOLLOW ANGLIA ADVISORS ON INSTAGRAM

This material represents a highly opinionated assessment of the financial market environment based on assumptions and prevailing information and data at a specific point in time and is always subject to change at any time. Although the content is believed to be correct at the time of publication, no warranty of its accuracy or completeness is given. It is never to be interpreted as an attempt to forecast any future events, nor does it offer any kind of guarantee of any future results, circumstances or outcomes.

The material contained herein is not necessarily complete and is also wholly insufficient to be exclusively relied upon as research or investment advice or as a sole basis for any financial decisions, including investment decisions or making any kind of consumer choices, without further consultation with Anglia Advisors or other qualified Registered Investment Advisor. The user assumes the entire risk of any decisions made or actions taken based in whole or in part on any of the information provided in this or any Anglia Advisors communication of any kind.

Under no circumstances is any of Anglia Advisors’ content ever intended to constitute tax, legal or medical advice and should never be taken as such. Neither the information contained or any opinion expressed herein constitutes a solicitation for the purchase of any security or asset class. No advice may be rendered by Anglia Advisors unless or until a properly-executed Client Engagement Agreement is in place.

Posts may contain links or references to third party websites or may post data or graphics from them for the convenience and interest of readers. While Anglia Advisors might have reason to believe in the quality of the content provided on these sites, the firm has no control over, and is not in any way responsible for, the accuracy of such content nor for the security or privacy protocols that external sites may or may not employ. By making use of such links, the user assumes, in its entirety, any kind of risk associated with accessing them or making use of any information provided therein.

Those associated with Anglia Advisors, including clients with managed or advised investments, may maintain positions in securities and/or asset classes mentioned in this post.

If you enjoyed this post, why not share it with someone or encourage them to subscribe themselves?